.png)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

Merchant underwriting is the risk assessment process that payment service providers, acquirers, and PayFacs use to evaluate businesses before allowing them to accept card payments. It involves verifying that a merchant is legitimate, financially stable, compliant with regulations, and unlikely to generate excessive fraud or chargebacks. Underwriting protects the payment ecosystem by identifying high-risk merchants early and preventing onboarding decisions that could lead to financial loss, regulatory sanctions, or card scheme penalties. While underwriting begins at onboarding, it continues as an ongoing function through transaction monitoring and periodic reviews. This article defines merchant underwriting, explains why it is required, and outlines what the process evaluates.

Definition of merchant underwriting

Merchant underwriting is the risk assessment conducted before a merchant is approved to process card payments. It determines whether a business presents acceptable financial, compliance, and operational risk. The underwriting decision results in approval, conditional approval with enhanced monitoring or reserves, or decline.

Underwriting evaluates multiple dimensions of risk: business legitimacy, financial viability, compliance with regulations and card scheme rules, and transaction risk based on industry, business model, and processing history.

The process is not a one-time event. Initial underwriting establishes baseline risk at onboarding. Ongoing monitoring and periodic reviews detect changes in merchant behavior, financial health, or external risk factors that may require re-evaluation.

When underwriting occurs

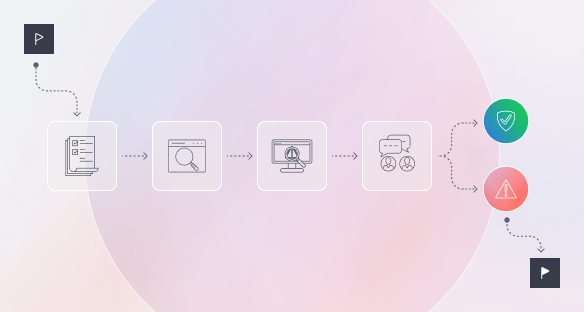

Underwriting occurs at onboarding when a merchant applies to accept card payments. The merchant submits an application with business information, ownership details, financial projections, and supporting documentation. The acquirer or payment service provider reviews the application, performs verification and screening checks, and makes an approval decision.

Underwriting continues after onboarding. Merchants are monitored continuously for transaction anomalies, chargeback increases, compliance issues, and adverse information. Triggered reviews occur when risk indicators surface. Periodic reviews reassess risk at defined intervals, particularly for high-risk merchants.

Why merchant underwriting is required

Card scheme rules and acquirer liability

Card schemes require documented underwriting programs. Visa's Acceptance Risk Standards (VARS), which replaced GARS in October 2024, and Mastercard's Security Rules mandate that acquirers verify merchant legitimacy, assess risk, and maintain ongoing oversight.

Acquirers are liable for merchant fraud, chargebacks, and compliance violations. When a merchant commits fraud or becomes insolvent, the acquirer absorbs financial losses. Card schemes hold acquirers accountable for merchant behavior. High chargeback rates or fraud levels trigger scheme monitoring programs, which carry fines, operational restrictions, and potential program termination.

Underwriting reduces this liability by identifying and declining high-risk merchants before they cause harm. Merchant acquiring institutions must balance growth objectives with robust risk controls to maintain healthy relationships with card schemes.

Regulatory and AML obligations

Anti-money laundering regulations require payment service providers to perform customer due diligence. The Financial Action Task Force (FATF) sets international standards requiring payment providers to verify customer identity, understand business activities, and monitor transactions for suspicious patterns.

Underwriting satisfies these obligations by verifying business legitimacy, identifying beneficial owners, screening against sanctions lists, and assessing transaction risk. Regulatory authorities expect documented underwriting policies, screening records, and audit trails.

Financial and reputational risk

Beyond regulatory compliance, underwriting plays a critical role in protecting financial performance and reputation. Merchants with elevated chargebacks and fraud rates drive refund and dispute costs that reduce margins and increase reputational risk. High-risk portfolios increase operational costs through monitoring, dispute management, and remediation efforts.

Reputational risk arises from association with fraudulent, unethical, or illegal merchants. Payment service providers that onboard high-risk merchants without adequate controls face scrutiny from schemes, regulators, and the public. Damage to reputation harms relationships with banks, partners, and customers.

What underwriting evaluates

Business legitimacy and ownership

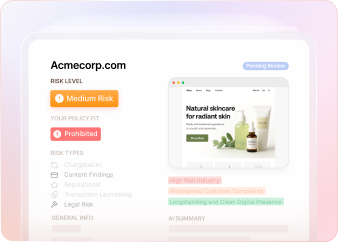

Underwriting verifies that the merchant is a legitimate, operating business. This includes confirming incorporation with government registries, validating the business address, and checking that the operating website matches the stated business and is functional.

Ownership verification identifies beneficial owners and ultimate controlling parties. This is required for sanctions screening and anti-money laundering compliance. Underwriters check ownership structures, verify principal identities, and flag complex or opaque ownership arrangements.

Financial viability

Financial assessment evaluates whether a merchant can sustain operations and absorb chargebacks and refunds by reviewing bank statements, cash flow, and revenue history. Stated volume projections are then compared against historical performance, with significant mismatches raising concerns about business maturity, scalability, or financial stability.

Underwriters assess the merchant's ability to absorb chargeback losses. Merchants with thin margins, inconsistent cash flow, or high debt levels present higher financial risk.

Compliance and sanctions screening

Compliance screening checks merchants and beneficial owners against sanctions lists maintained by regulatory authorities worldwide. Matches result in immediate decline unless a false positive can be confirmed.

Politically exposed person (PEP) screening identifies individuals with significant public or political positions. PEP status does not automatically disqualify a merchant but triggers enhanced due diligence.

Adverse media screening searches for negative news, regulatory actions, fraud allegations, or reputational issues associated with the merchant or its owners. Findings require manual review and judgment.

Industry validation confirms the merchant's category is not restricted or prohibited by card schemes, acquirers, or regulators.

Transaction and fraud risk

Transaction risk assessment examines average ticket size, transaction frequency, refund rates, and chargeback history. High-ticket transactions, high refund rates, or prior chargeback issues increase risk scores.

Business models that increase customer disputes or fraud exposure are flagged. Card-not-present transactions, recurring billing, future delivery services, and cross-border processing carry elevated risk. Underwriters evaluate whether the merchant's fraud prevention controls are adequate for their business model.

Understanding what traditional scoring approaches miss helps risk teams build more effective evaluation frameworks that detect subtle indicators of merchant risk.

Who performs underwriting

Acquirers and sponsor banks

Direct acquirers underwrite every merchant individually. Each merchant receives a unique merchant identification number and is subject to direct scheme oversight. The acquirer assumes full liability for merchant behavior.

Sponsor banks underwrite payment facilitators and may audit the PayFac's sub-merchant underwriting program. The sponsor bank retains ultimate liability and may impose portfolio restrictions or monitoring requirements on the PayFac.

PayFacs and payment facilitators

Payment facilitators underwrite sub-merchants under their master merchant account. PayFacs perform the underwriting steps but operate under the sponsor bank's oversight. The sponsor bank audits the PayFac's underwriting policies, screening procedures, and monitoring capabilities.

PayFacs balance speed and risk quality. Fast onboarding processes attract sub-merchants, but poor underwriting increases portfolio risk and may result in sponsor bank intervention.

Third-party underwriting services

Some acquirers outsource underwriting to third-party providers or use technology platforms to automate verification and screening. Third-party services do not assume liability but provide data, tools, and recommendations to support underwriting decisions.

The acquirer retains final approval authority and liability regardless of third-party involvement.

Underwriting as an ongoing function

Initial onboarding vs. continuous monitoring

Initial underwriting at onboarding establishes baseline risk. It determines whether the merchant is legitimate, compliant, and financially viable at the time of application.

Continuous monitoring detects changes after onboarding. Merchants may shift business models, change ownership, expand into higher-risk categories, or experience financial distress. Transaction patterns may deviate from projections. Adverse information may surface through media, complaints, or regulatory actions.

Effective underwriting programs treat monitoring as a continuation of underwriting, not a separate function. Automated cross-referencing helps risk teams identify related entities, detect business model changes, and surface indicators of transaction laundering before they escalate into scheme compliance issues.

Triggered reviews and re-underwriting

Triggered reviews occur when risk indicators surface. Volume spikes, chargeback rate increases, customer complaints, adverse media, or changes in ownership prompt re-evaluation. The merchant may be required to submit updated documentation, explain transaction anomalies, or accept enhanced monitoring terms.

Re-underwriting reassesses whether the merchant still meets approval criteria. If risk has increased beyond acceptable levels, the acquirer may impose reserves, reduce volume limits, or terminate the relationship.

Building underwriting programs that scale

As merchant portfolios grow, manual underwriting becomes unsustainable. Organizations need systems that maintain decision quality while accelerating low-risk approvals. Ballerine's merchant risk platform enables risk teams to automate routine verification, continuously monitor merchant behavior, and surface complex risks for expert review. This approach reduces false positives, speeds legitimate merchant onboarding, and helps organizations stay ahead of evolving fraud patterns.

Merchant underwriting is the risk assessment that protects payment service providers, acquirers, and card schemes from fraud, chargebacks, and regulatory violations. It evaluates business legitimacy, financial stability, compliance, and transaction risk. Underwriting begins at onboarding and continues through ongoing monitoring and periodic reviews. Effective underwriting balances speed, accuracy, and risk quality to support safe, sustainable portfolio growth.