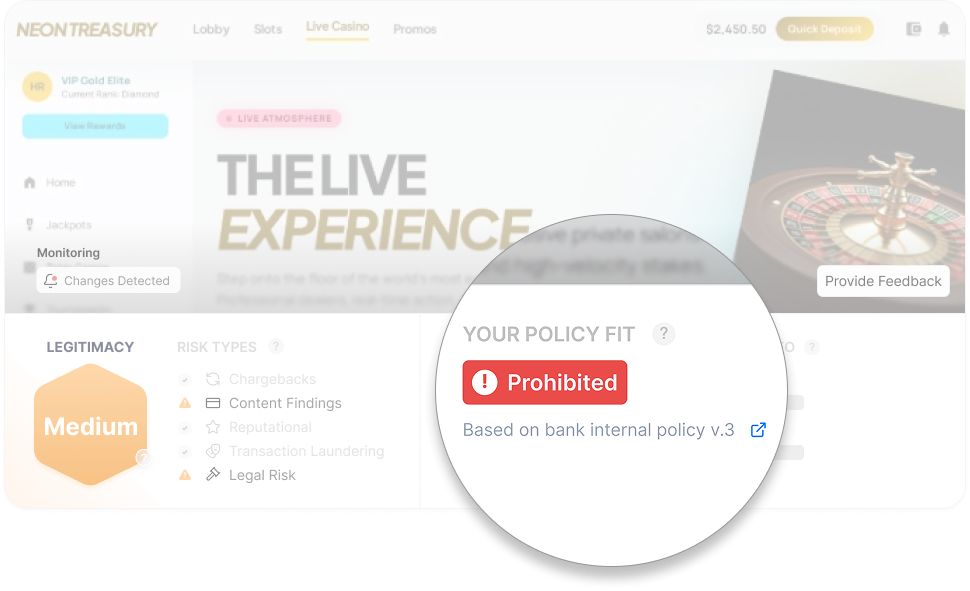

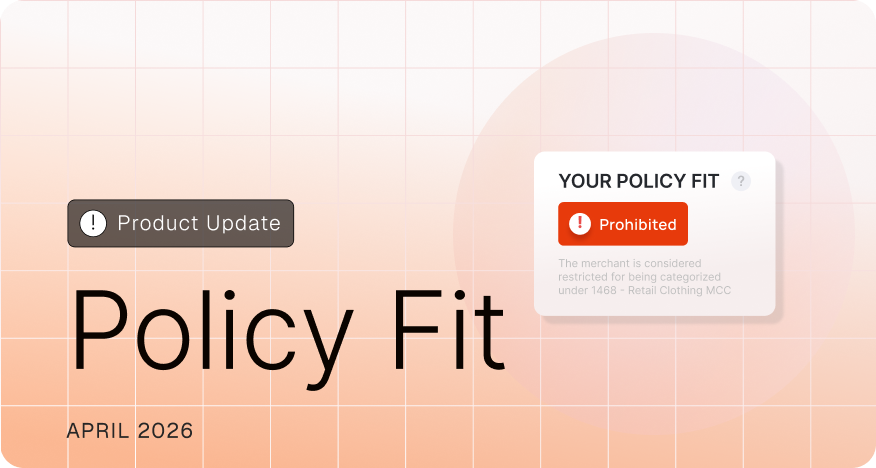

Ballerine introduces Policy Fit, a policy decision layer inside Digital Footprint.

Policy Fit allows financial institutions to upload their own Acceptable Use Policy and automatically evaluate merchants against it. Instead of relying only on generic industry rules, financial institutions receive a policy-specific verdict, with reasoning tied directly to the merchant’s actual profile.

Baseline industry requirements such as scheme rules, regulatory compliance, and fraud prevention are already well understood and widely enforced. These fundamentals are fully covered by Ballerine’s core Digital Footprint analysis.

The challenge begins above that baseline.

Each financial institution has its own policy preferences shaped by geography, operational complexity, regulatory exposure, and vertical focus. Two financial institutions can agree on the same risk facts and still reach different decisions because policy is not risk.

In today’s market, even semi-automated onboarding flows still require a dedicated manual policy review step. Custom policy interpretation remains a human milestone that sits outside automated risk checks, creating friction, delays, and inconsistency.

Policy Fit evaluates merchants against your Acceptable Use Policy using Digital Footprint signals such as:

The output is a clear policy verdict:

Each verdict includes clear reasoning explaining which policy rules were triggered and why.

Clients share internal policy guidelines and or a public AUP, such as Stripe’s public Acceptable Use Policy¹. These documents are ingested into Ballerine’s model and processed by an LLM-driven workflow that converts them into structured, executable policy rules.

The model highlights ambiguous areas and edge cases. Together with Ballerine’s customer success team, clients review the generated policy logic and validate it using known test cases and stress scenarios. This ensures version one of the policy implementation is complete and accurate before activation.

Once active, every merchant is automatically evaluated against the policy using Digital Footprint data. The result is a clear verdict with attached reasoning, ready for operational use.

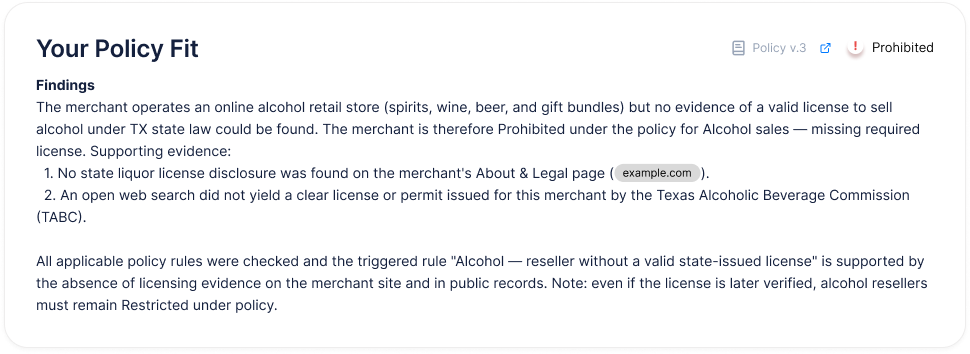

A merchant selling alcohol is missing a required state license.

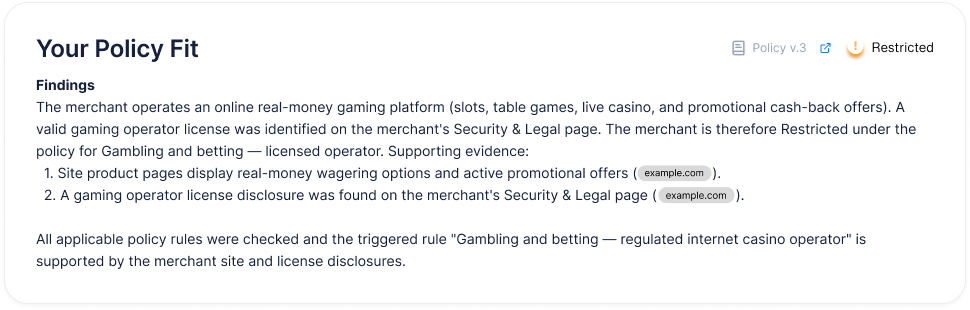

A merchant operating an online real-money casino holds a valid gaming license.

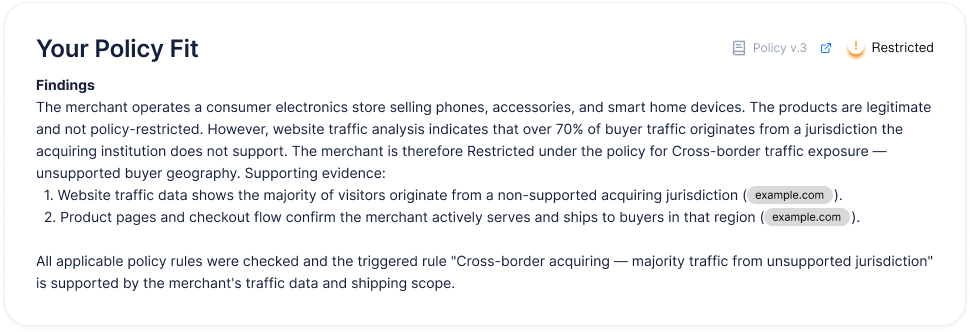

A merchant sells legitimate consumer electronics, but the majority of buyer traffic originates from a country the acquiring institution does not support.

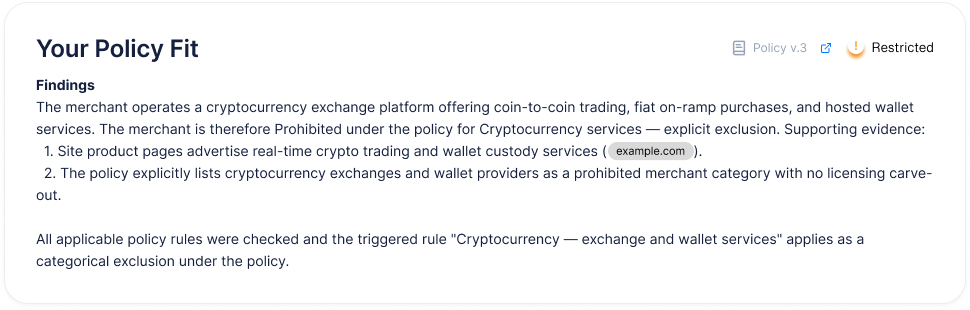

A merchant offers cryptocurrency exchange and wallet services.

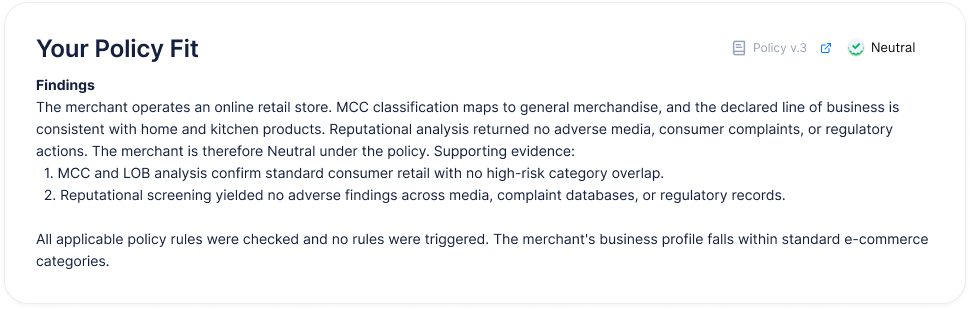

A merchant sells everyday consumer goods with no policy-flagged categories or risk signals.

Policy Fit turns Acceptable Use Policies into a fast, dynamic, and explainable decision engine.

Instead of relying on slow, manual policy interpretation, financial institutions gain:

Most importantly, it reflects a simple truth:

Good risk decisions are not one-size-fits-all and policy decision engines should not be either.

--- ---

¹ Ballerine uses Stripe’s publicly available Acceptable Use Policy as an illustrative example only. This does not indicate any partnership or collaboration between the companies.

.png)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.png)

.png)