Related Questions

Why does Mastercard MMSP matter for acquirers and PayFacs?

How is MMSP different from merchant onboarding?

What should an MMSP-ready monitoring workflow include?

How can acquirers prepare for Mastercard MMSP expectations?

.png)

An MMSP (Merchant Monitoring Service Provider) is a Mastercard-approved provider engaged by an acquirer to perform BRAM (Business Risk Assessment and Mitigation) monitoring and merchant transaction laundering detection on the acquirer's behalf as part of participation in the Merchant Monitoring Program.

Acquirers engage MMSPs directly to fulfill their monitoring obligations under Mastercard's Merchant Monitoring Program. Payment service providers (PSPs) and payment facilitators (PayFacs) depend on the acquirer's MMSP design while still carrying portfolio risk for the merchants they board and service.

Mastercard introduced the MMSP designation to standardize monitoring quality across the acquiring ecosystem. Before formalized MMSP requirements, monitoring approaches varied widely, creating blind spots in merchant activity oversight. The MMSP framework moves acquirers from policy statements to evidence-based oversight with consistent detection standards and documented outcomes.

The MMSP model operates through a structured engagement between acquirer and approved service provider:

Registration and approval: The acquirer confirms that the MMSP is approved by Mastercard for performing BRAM monitoring or transaction laundering monitoring services, then registers the MMSP as a service provider in accordance with Mastercard Rules.

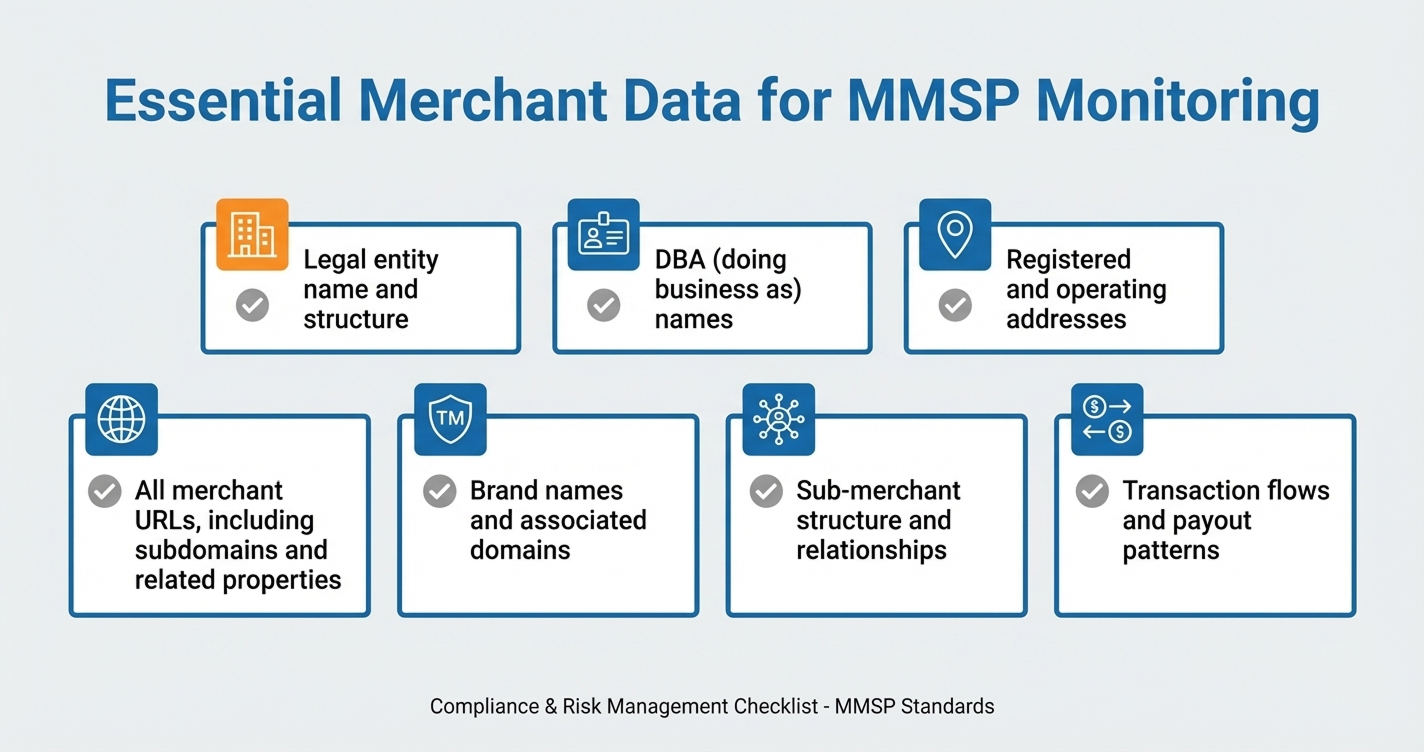

Data submission: The acquirer provides the MMSP with complete merchant information including legal names, doing business as names, addresses, and all URLs. Incomplete data creates monitoring gaps.

Initial scanning: The MMSP performs an initial scan of the merchant's activities to identify potential violations before the merchant processes transactions. This scan covers website content, product offerings, regulatory compliance signals, and transaction laundering indicators.

Persistent monitoring: The MMSP continuously monitors each merchant's activities for BRAM violations and transaction laundering. Monitoring must include all merchant URLs, including restricted members-only areas unless prohibited by law.

Violation reporting: When the MMSP identifies potential violations, it reports them to the acquirer within five business days. Reports include evidence artifacts, time-stamped documentation, and clear rationale.

Acquirer investigation: The acquirer investigates reported violations within 15 calendar days, ensures that all violating activities cease, and reports the resolution back to the MMSP.

Monthly reporting: The acquirer provides Mastercard with unaltered monthly reports generated by the MMSP, detailing monitored merchants and identified violations.

MMP (Merchant Monitoring Program) is Mastercard's voluntary program that defines the expectations, standards, and assessment framework for how acquirers must oversee merchant activity to prevent BRAM violations and transaction laundering.

Who participates in MMP: MMP is designed for acquirers who choose to participate in the program. Participation is voluntary, but acquirers that fully participate and meet all program requirements may be eligible for assessment mitigation related to BRAM violations. Acquirers that process transactions for merchants that have undergone initial scans and are being persistently monitored by an approved MMSP for BRAM or transaction laundering violations can qualify for these mitigations.

MMSP is the execution layer that enables compliance with those expectations. An MMSP is the approved service provider that performs the actual monitoring, detection, and reporting on behalf of the acquirer.

Participation in MMP requires real monitoring, not policy documentation. Acquirers must engage one or more Mastercard-approved MMSPs, register them as service providers, and ensure they perform both initial scans and persistent monitoring. The quality of merchant data provided to the MMSP, the completeness of URL coverage, and the depth of monitoring directly affect compliance outcomes.

Monitoring depth equals portfolio risk exposure. Shallow monitoring increases the likelihood of undetected violations, which leads to remediation burdens, assessments, and potential program penalties. Evidence quality determines audit defensibility. When Mastercard issues a BRAM notification, acquirers must submit an unaltered incident report created by the MMSP, demonstrating when the merchant was provided to the MMSP, confirmation of ongoing monitoring, any alerts generated, and actions taken.

If violations were not detected, the acquirer must explain why and how future detection will improve. Without strong MMSP execution, these explanations become difficult to defend.

Effective MMSP monitoring extends beyond homepage scans. It includes open web content, deep web resources, and relevant restricted areas such as member portals, gated content, and login-protected pages. Surface-level crawling misses where violations often hide.

Strong MMSP services map licensing and regulatory obligations by geography and business model. This goes beyond MCC (Merchant Category Code) classification or high-level line-of-business tagging. It requires understanding what regulatory frameworks apply to specific merchant operations, what licenses are required, and whether the merchant holds them.

Transaction laundering detection validates whether what a merchant sells on their website matches what they process through the payment network. It identifies undisclosed third-party selling, sub-merchant behavior, fulfillment mismatches, and ownership patterns that indicate front companies or pass-through structures.

Every finding must be supported by captured artifacts, time-stamped snapshots, and clear rationale. This evidence forms the foundation of incident reports, audit responses, and scheme inquiries. Without it, decisions cannot be defended.

MMSP-grade monitoring must support rapid onboarding checks and continuous monitoring without manual queues. Waiting days for initial scan results creates onboarding delays. Slow continuous monitoring means violations go undetected longer, increasing exposure.

To enable effective MMSP monitoring, acquirers and PSPs must provide complete merchant data:

Incomplete data creates monitoring gaps. Missing URLs mean undetected violations. Shallow entity information prevents ownership analysis.

Ensure every new merchant undergoes an initial scan before processing their first transaction. This satisfies Mastercard's January 2026 requirement and creates a clean entry gate. Modern merchant onboarding systems can perform these scans without creating bottlenecks.

Apply ongoing surveillance based on merchant risk tier, MCC category, or transaction volume. High-risk merchants require more frequent monitoring. Merchant monitoring platforms enable risk teams to configure monitoring frequency by segment.

Define clear processes for when violations are detected: investigation timelines, evidence collection, merchant communication, and resolution documentation. Teams often struggle with this phase because traditional scoring misses fast-moving merchant risks.

Violations often hide in product catalogs, member areas, and checkout flows. Shallow scanning misses the content that creates exposure.

MCC codes provide a starting point, not a complete risk picture. Many violations occur when merchants operate outside their stated MCC or when the MCC itself is too broad to capture regulatory nuance.

Without captured artifacts and time stamps, decisions cannot be defended. If Mastercard asks why a violation was not detected, claiming you checked the site is not sufficient.

If monitoring data is not retained or if there is no clear rationale for why a merchant was approved or flagged, audit responses become guesswork.

As a certified MMSP partner, Ballerine performs automated MMSP scans in minutes, enabling risk checks without slowing merchant onboarding. New merchants are evaluated with the depth required by Mastercard's January 2026 standards for initial scans.

Ballerine's AI agents validate licensing and regulatory signals per region and business model. This goes far beyond surface-level classification. The system identifies what regulatory frameworks apply, what licenses are required, and whether the merchant holds them. This depth prevents misclassification and reduces false negatives through merchant underwriting.

Ballerine validates website content against transaction behavior, ownership and entity signals, and fulfillment and customer journey consistency. It identifies discrepancies between what the merchant claims to sell and what they actually process, surfacing hidden sub-merchants, undisclosed third-party sellers, and pass-through structures through transaction laundering detection.

Ballerine is designed to surface hidden changes in merchant behavior over time through merchant monitoring. It detects new product lines, shifts in geographies, changes in fulfillment patterns, and alterations to restricted content. This aligns with Mastercard's direction toward deeper ongoing coverage beyond initial scans.

Every decision includes defensible evidence and clear rationale. Risk summaries, policy mappings, evidence packs, and recommended actions are structured for reviews and scheme inquiries. When Mastercard requests an incident report, the documentation exists and is traceable.

Disclaimer: The information presented in this article is provided for general educational purposes only and is not endorsed by, affiliated with, or issued by Mastercard. While Ballerine strives to ensure accuracy, Mastercard retains sole authority over the interpretation and application of its rules, programs, and standards.Readers should consult the official Mastercard Rules, Security Rules and Procedures, and applicable program documentation, as published by Mastercard from time to time, for definitive and binding requirements.

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

edited%205.webp)